- calendar_today August 31, 2025

If you’re living in Michigan and dealing with student loans, 2025 is already shaping up to be a year of big changes. New federal regulations are affecting how borrowers repay loans, access forgiveness, and even how much students can borrow in the future.

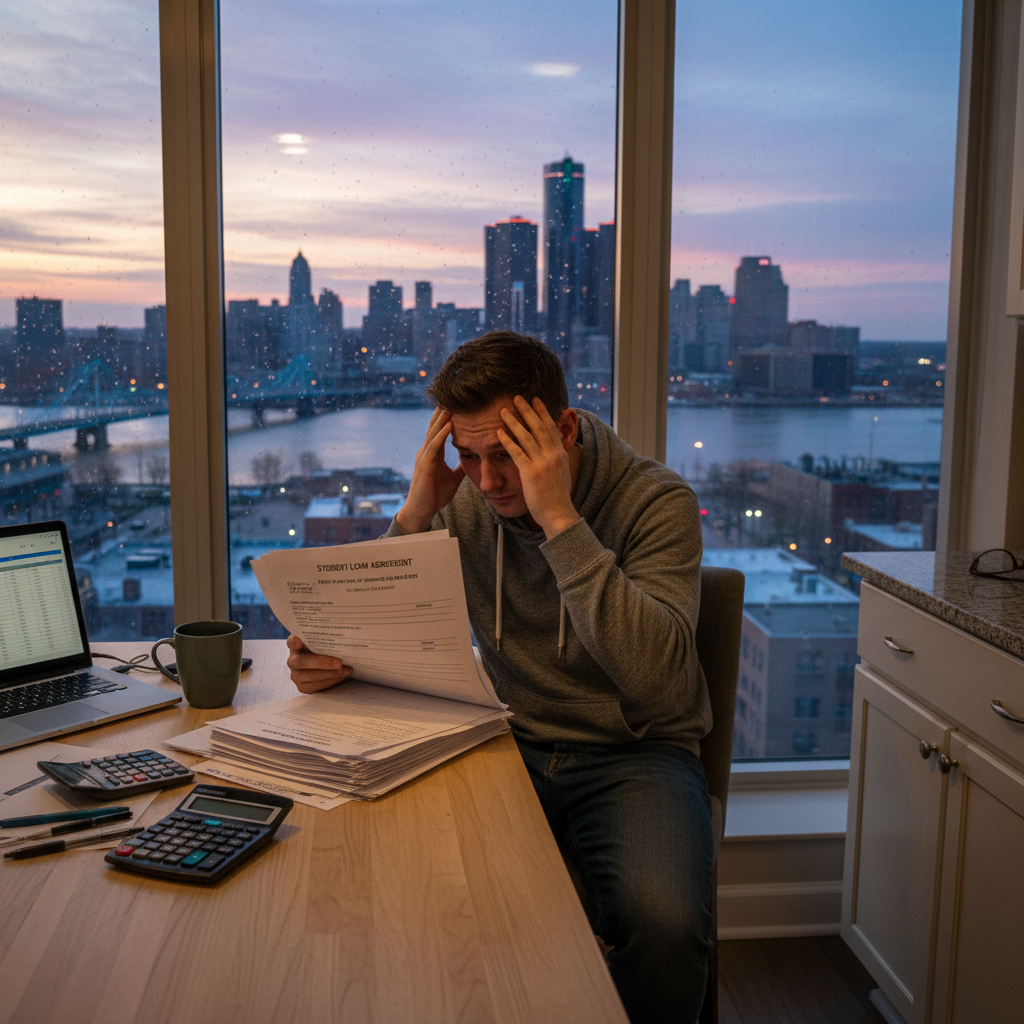

From Detroit and Ann Arbor to Grand Rapids and Marquette, thousands of Michiganders are facing a stricter, less flexible system than before. Whether you’re a recent graduate from University of Michigan, a public servant in Lansing, or a parent with kids about to start college, understanding the new system is critical.

Here’s what’s changed—and what it means for you.

1. Interest Is Back—and Balances Are Climbing

One of the biggest updates is the return of interest charges on federal student loans. For the past few years, borrowers enjoyed a break during the pandemic pause. But starting August 2025, all federal student loans are once again accruing interest.

This means if you’re not paying down the principal fast enough, your balance is growing again—sometimes by hundreds of dollars a month. For many Michigan borrowers, especially those with balances above $25,000, this is adding noticeable pressure to monthly budgets.

Cities like Flint, Saginaw, and Kalamazoo, where wages often trail the national average, are already seeing more borrowers struggling to keep up.

2. Fewer Repayment Plans—and Longer Forgiveness Timelines

Another major shift in 2025 is a reduction in repayment plan options. Previously, you could choose from plans like SAVE, PAYE, REPAYE, IBR, and more.

Now, most of those are gone.

Borrowers must now pick between:

- A standard 10-year plan, or

- A new income-driven option called the Repayment Assistance Plan (RAP)

While the RAP plan adjusts payments based on your income, it comes with a longer path to forgiveness. Instead of 20 or 25 years, some borrowers may need to make payments for up to 30 years before the remaining balance is wiped away.

For many Michiganders who counted on earlier forgiveness—especially in public sector roles—this means reassessing long-term plans. Teachers in Detroit, nurses in Traverse City, or city workers in Lansing may now need to remain in repayment far longer than they expected.

3. Collections Are Back for Those in Default

The grace period for defaulted student loans is over. In 2025, the government has resumed collections on overdue accounts.

If you’re behind on your payments, you could now face:

- Wage garnishment

- Seized tax refunds

- Offset Social Security payments (for older borrowers)

This is hitting Michigan residents hard in areas with higher unemployment or limited job markets—especially in parts of northern Michigan and the Upper Peninsula.

To avoid these consequences, borrowers are being urged to look into loan rehabilitation or consolidation as soon as possible. These tools can bring your loans back into good standing and prevent aggressive collection tactics.

4. Public Service Forgiveness Just Got Stricter

If you’ve been working in a government or nonprofit role in Michigan—say, as a public school educator, city official, or social worker—you were probably counting on Public Service Loan Forgiveness (PSLF).

While PSLF is technically still active in 2025, it now comes with stricter rules:

- You must be enrolled in the new RAP plan

- Older plans like PAYE or IBR no longer qualify

- Previous qualifying months may be voided unless you consolidate and switch

This means that workers in Ann Arbor’s public schools, Wayne County hospitals, or nonprofits in Grand Rapids could see their progress toward forgiveness erased if they don’t take action.

Unfortunately, the Department of Education has a backlog in processing forgiveness applications, so delays are expected even after you meet the requirements.

5. Borrowing Limits Will Affect Future Students

Families across Michigan are also dealing with new caps on how much students (and their parents) can borrow.

Starting in 2025:

- Parent PLUS loans are limited to $65,000 per student

- Graduate federal loans are capped at $100,000 to $200,000, depending on the program

This has serious implications for families sending kids to private schools like Kalamazoo College, Hillsdale, or even out-of-state universities.

Even in-state flagship schools like the University of Michigan and Michigan State now leave some students needing private loans to cover the difference—often at higher interest rates with fewer protections.

As a result, many Michigan families are rethinking college choices altogether—opting for community colleges, trade schools, or hybrid programs to reduce debt from the beginning.

What You Can Do Now

If you’re worried about these changes, you’re not alone. Michigan borrowers are facing uncertainty, but there are ways to stay ahead:

- Double-check your loan servicer account and ensure you’re on the correct repayment plan

- If you work in public service, verify your PSLF status and switch to RAP if needed

- For defaulted loans, explore consolidation or rehabilitation before collections hit

- If you’re planning college soon, compare total costs and borrowing needs up front

Finally, talk to a certified student loan advisor or financial counselor—especially if your situation is complex. Michigan has local nonprofit agencies that offer free or low-cost guidance to help you create a repayment strategy that fits your budget.

Michigan’s student loan borrowers are navigating a tighter system in 2025. Interest charges are back, forgiveness takes longer, and borrowing limits are shrinking.

But staying informed is half the battle. Whether you’re in Detroit, East Lansing, Marquette, or Grand Rapids, making smart decisions now can help you avoid long-term financial strain.

These changes may feel overwhelming, but they don’t have to derail your future. Knowledge is power—and preparation is key.